19 MAY 2024

Things are ticking along nicely here in the Newcastle property market. Across the Newcastle LGA, the median house price in March has increased to $885,000, which is up a solid 2.3% from the same time a year ago. We are now approaching the peak, which was set back in mid-2022 before interest rates cooled the market.

These figures are encouraging for homeowners, especially those who purchased at the top of the market. But they are also lower than across most capital city markets. Data provider Core Logic reports that prices (at the end of March) across the country are up 8.8%. Perth continues to be the standout area with 19.8% growth, and Hobart (at 0.3%) is the weakest.

On the ground, we are seeing plenty of interest from first-home buyers, upgraders, and downsizers. There aren’t a lot of investors in the market, and while there are still Sydneysiders making the journey north, they are in smaller numbers than a few years ago. The first quarter of 2024 has seen an influx of new listings, but there is enough demand from buyers to soak up this additional supply.

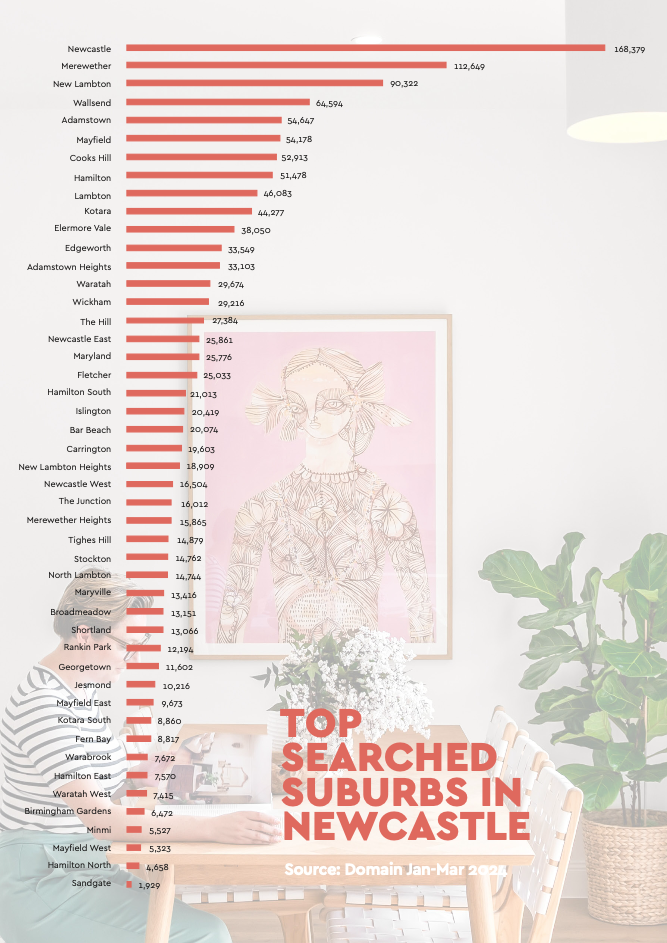

In this issue, we have included how prices have changed by suburb over the last ten years. These statistics are for house prices only (and only where the number of sales made the statistics somewhat reliable).

Usually, we only focus on the inner areas of Newcastle, but every so often it is good to widen the lens and look at areas further afield.

Hamilton South and Bolton Point couldn’t be further apart geographically and financially, but they are the standout locations at this time.

Locations near water feature heavily at the top of the list, particularly in the Lake Macquarie region, with areas like Swansea, Coal Point, Dora Creek, Fennell Bay, Belmont and Marks Point performing well.

The rest of the results are a little mixed, making major conclusions challenging to draw.

The average between these areas shows price growth of 113%. Good for those who have already purchased. But not great for those looking to get into the market. Ten years ago you could have picked up an average house in Merewether for $840,000, whereas now you’d be looking at over $2 million. And you could have bought the average home in Gateshead for $315,000. But given the influx of new people into Newcastle, that commute into town would most likely be twice as long.

One thing that stands out for us is the relative decline in interest in the areas around the University. A decade ago, people were buying investment properties in the area and renting them out to students. Nowadays, they are selling those properties, and first-home buyers are moving in.

While that has been good for the area's gentrification, it means those big spending investors (often from Sydney) are not paying top prices. Part of that could be interest rates and the lack of investors in the market in recent years. But also, the Uni has built plenty of on-campus accommodation during that time.

The new facility in Hunter Street and more online learning means students no longer need to be within walking distance. In addition, there is plenty of townhouse development in the area, which means there is a surplus of options. Two suburbs in particular (Jesmond and Birmingham Gardens) have seen the lowest growth during this time.

Teralba has seen risen sharply, no doubt due to the new homes being built in the area.

Get the latest real estate tips and advice on buying, selling & investing on properties.